IGMIN: We're glad you're here. Please click 'create a new query' if you are a new visitor to our website and need further information from us.

If you are already a member of our network and need to keep track of any developments regarding a question you have already submitted, click 'take me to my Query.'

Welcome to IgMin Research – an Open Access journal uniting Biology, Medicine, and Engineering. We’re dedicated to advancing global knowledge and fostering collaboration across scientific fields.

At IgMin Research, we bridge the frontiers of Biology, Medicine, and Engineering to foster interdisciplinary innovation. Our expanded scope now embraces a wide spectrum of scientific disciplines, empowering global researchers to explore, contribute, and collaborate through open access.

Welcome to IgMin, a leading platform dedicated to enhancing knowledge dissemination and professional growth across multiple fields of science, technology, and the humanities. We believe in the power of open access, collaboration, and innovation. Our goal is to provide individuals and organizations with the tools they need to succeed in the global knowledge economy.

IgMin Publications Inc., Suite 102, West Hartford, CT - 06110, USA

The currently existing Russian and other legislation, as well as special literature, do not contain a methodology for the formation of the business reputation of the organization’s personnel and as a result, there is no unambiguous perception of the business, professional qualities of personnel as an object of evaluation of the organization in the market system. Therefore, it is impossible to single out the share of the results of intellectual advantage in the goods and services produced.

This confirms the requirements formulated in paragraph 4 of Accounting Regulation 14/2007 «Accounting for intangible assets», which states that the intellectual and business qualities of the organization’s personnel, their qualifications, and their ability to work are not included in the intangible assets (since they are inseparable from their carriers and cannot be used without them).

Meanwhile, the interests of the leading economically developed countries of the world lie in the field of accelerated growth of knowledge acquisition and application of professional skills. This trend of development of economically developed countries forms the basis of competitiveness and efficiency of their work.

It should be noted that in the world economy, there is insufficient theoretical elaboration and a special practical significance and relevance of the issue of assessing the business reputation of the personnel of an economic entity.

The article presents a comprehensive methodology for evaluating the performance of industrial and production personnel (the standard-production methodology), which contributes to the formation of accounting and information support for the analysis of the activities of both structural divisions, responsibility centers, business segments and commercial organizations as a whole. The author’s standard-production methodology makes it possible to determine the business reputation of industrial and production personnel, which contradicts the official economic paradigm.

The problem of business valuation

After the translation into Russian of the bestseller «The Value of Companies: Evaluation and Management» by McKinsey partners, the ideas proposed by the authors have become actively discussed in Russia. For example, a few years ago, as the head of Lukoil Overseas, Andrey Kuzyaev bought up promising fields for LUKOIL in the Komi Republic, Uzbekistan, Kazakhstan, Azerbaijan, and Egypt. During this time, LUKOIL’s capitalization has grown tenfold. The thesis of the priority of the task of maximizing value in the interests of shareholders has become dominant in global business circles and there has been a steady interest in the concept and methods of the cost approach to management.

The strategy of most companies at a certain stage of their development will necessarily focus on preparing for the sale of the business. At this point, the work on increasing the value of the company, identifying those indicators that will be used by potential buyers to assess this value, comes to the fore. The next obvious step is to focus the company’s work on maximizing the values of these indicators.

Today, when companies enter the international stock market and attract large foreign investments, mergers, and acquisitions, the problem of managing the company’s value is put at the forefront [11Filatov EA. Management of the production cost of an industrial enterprise. Bulletin of IrSTU. Irkutsk: Publishing House of IrSTU. 2006; 2(26):2;35-36.-44Shchadov MI, Filatov EA. The Relevance of the methodology for the assessment of business reputation of the human capital of the organization. Vestnik of the Irkutsk. Irkutsk: publishing house of Irkutsk state technical university. 2007; 1:1(29); 241-242.]. A number of companies are acquired for further resale, and the shareholder sets the management the main task: to increase the value of the company. The owner considers the purchase of the company as a medium-term or long-term investment.

For example, the world’s largest manufacturer of chewing gum and lollipops, Wrigley, acquired an 80 % stake in the Russian confectionery company «A. Korkunov» for $ 300 million. Due to this, the American corporation entered the segment of chocolate production. The Americans estimated the entire Odintsovo confectionery factory at $ 375 million, which is 3.7 times more than the annual turnover and 21 times more than the profit. According to American businessmen, it is possible to enter a steadily growing market only through the acquisition of existing brands. Therefore, one of the richest entrepreneurs on Earth constantly sells his shares, over the past five years, his share in the company has decreased by about half. By April 2006, Bill Gates owned only 9.4 % of Microsoft shares. In the mature competitive markets of the world, the following trend is observed: the more expensive the business or the larger the capitalization, the smaller the role of individual shareholders in it.

More and more Russian capitalists are changing their shares to increase the value of their companies, and the concentration of capital in the economy has begun to decline. The trend of changing the approach to value management is the assessment of the company’s performance as an investment project. The structure of the market changes quite quickly and there are a few examples of a business that has been held in the same hands for a long time. Companies are looking for large investors, to merge and change their owners. And even if the owner does not have the purpose of reselling the business today, such a proposal can be considered at any time. The company’s realizable value consists of its book value and goodwill. The company’s intangible assets have a large impact on the business value: the knowledge and experience of the staff, ownership of trademarks, geographical location, established relationships with suppliers and customers, and technological know-how. When managing the company’s value, managing intangible assets and increasing their value can significantly affect the total amount of business sales.

One of the definitions of goodwill adopted by the American Society of Appraisers (ASA) is the «good name» of the firm, which includes the intangible assets of the company: business reputation, location, customer relationship, level of training of personnel, etc. Intangible assets can be divided into three groups:

Non-amortized assets with an indefinite term. Intangible assets inseparable from the company: trained personnel, achievements in product promotion, geographical location, reputation;

Also, non-amortized assets that have an indefinite term, but are inseparable from the company’s personnel: the reputation and professional skills of employees, commercial abilities, etc.;

Amortised assets that have a defined service life. Intangible assets that can be put on the balance sheet of the company: are trademarks, copyrights, and patents. An asset that can be valued separately.

The intellectual or human capital of a company has a large weight in the total value of intangible assets. The study of the influence of intellectual potential on business has been conducted for a long time. P. Drucker, a classic of modern management, argued that in the «knowledge society», the basic economic resource is knowledge, not natural resources or tangible assets. The same is said by the Russian professor, former Deputy Minister of Foreign Affairs of the Russian Federation, Fyodor Shelov-Kovedyaev, who says that it is human capital, not minerals, that is the main resource.

Meanwhile, these real assets (the company’s personnel) are not separately allocated and/or not evaluated in the company’s financial statements, but serve as a real source of profit. The structure of the intellectual capital of individual companies with different businesses may differ significantly. In particular, due to the structure of human (intellectual) capital from 1984 to 1994, IBM and DEC lost $ 55 billion in capitalization, while Microsoft, Intel, EDS, and Novell earned $ 80 billion. The task of the company’s management is to identify and manage these resources since the intellectual capital of the company is the most powerful engine of production. As a result, the most urgent question arises: how to manage processes that cannot be measured? Ignoring the value of the company’s business reputation and human capital limits the objectivity of making decisions on investing in the company’s business. For example, the readiness and professionalism of the company’s personnel, according to many economists, can be assessed by such indicators as the level of education for various groups of employees (engineering and technical workers, workers), staff turnover, and average work experience in the company.

Evaluation of the results of the IPP (Industrial and Production Personnel) as an association of many people performing various functions, it requires different approaches. Hence, an important methodological issue in the formation of the methodology for assessing the performance of commercial organizations for the purposes of assessing capitalization is the study and measurement of the influence of factors on the value of the studied economic indicators.

The author’s conceptual framework for assessing the business reputation of industrial and production personnel

The currently existing Russian and other legislation, as well as special literature, do not contain a methodology for forming the business reputation of the organization’s personnel, and as a result, there is no unambiguous perception of the business and professional qualities of the personnel as an object of evaluation of the organization in the market system. Therefore, it is impossible to distinguish the share of the results of intellectual advantage in the goods and services produced.

This confirms the requirements set out in paragraph 4 of the Accounting Regulations 14/2007 «Accounting for intangible assets», which states that intangible assets do not include the intellectual and business qualities of the organization’s personnel, their qualifications, and ability to work (since they are inseparable from their carriers and cannot be used without them).

Meanwhile, the interests of the leading economically developed countries of the world lie in the field of accelerated growth in the acquisition of knowledge and the application of professional skills. This trend in the development of economically developed countries is the basis of competitiveness and efficiency of their work.

It should be noted that in the world economy, there is a lack of theoretical development and a special practical significance and relevance of the issue of assessing the business reputation of the personnel of an economic entity.

Thus, the Accounting Regulation 14/2007 does not give a special definition not only of the concept of «business reputation of personnel», but also of the «intangible assets» themselves, but only approves the signs that the object of intangible assets must simultaneously correspond to.

To eliminate the information vacuum in the definition of the business reputation of the staff, let us first consider what the term business reputation itself implies.

The business reputation of an organization in the structure of intangible benefits is allocated according to Article 150 of the Civil Code of the Russian Federation. In the most general form, business reputation implies a formed opinion about the qualities (advantages and disadvantages) of a team, organization, enterprise, institution, or a particular individual in the business world.

Paragraph 21 of IAS 12 «Income Taxes» by business reputation implies the excess of acquisition costs over the buyer’s share of the fair value of the acquired identifiable assets and liabilities.

Paragraph 27 of the Accounting Regulations 14/2007 implies that the business reputation of an organization can be determined in the form of the difference between the purchase price of the organization (as an acquired property complex as a whole) and the value on the balance sheet of all its assets and liabilities.

The positive business reputation of the organization should be considered as a premium to the price paid by the buyer in anticipation of future economic benefits and should be considered as a separate inventory item.

The negative business reputation of the organization should be considered as a discount from the price provided to the buyer due to the lack of factors of stable buyers, reputation for quality, marketing and sales skills, business connections, management experience, staff qualification level, etc., and be considered as future income.

Paragraph 42 of the Accounting Regulations 14/2007 states that the value of the acquired business reputation of an organization is calculated as the difference between the amount paid to the seller for the organization and the amount of all assets and liabilities on the balance sheet of the organization at the date of its purchase (acquisition).

It follows that business reputation:

An intangible asset that has the following characteristics:

The absence of a material (physical) structure;

The possibility of identification (allocation, separation) by the organization from other property;

Use in the production of products, in the performance or provision of services, or for the management needs of the organization and others.

Occurs only in the case of the sale (purchase) of the economic entity as a whole;

The difference (positive, negative, nothing is said about zero) between the purchase price (the market valuation of the total assets of the organization) and the actual price of the economic entity (the sum of the individual market prices of the assets of the organization being sold).

Shows the reputation of the acquired company, its connections, and favorable (unfavorable) location.

Before entering the definition of the business reputation of the staff, it is necessary to enter the characteristics characteristic of the business reputation of the staff:

- Intangible asset;

- Occurs only in the case of income (revenue from the sale of products) of the business entity as a whole, as a result, it can be reflected annually in the financial statements;

- The difference (positive, negative, zero) between the professional qualities of personnel that show the level of competitiveness of labor productivity in comparison with the standard (average, market) level of labor productivity in a similar market sector;

- Shows the reputation of the staff, and the distinctive features of the staff in the labor market.

How can we not recall the well-known expression of Stalin (Dzhugashvili) Iosif Vissarionovich: «Cadres decide everything».

As a result, personnel reputation management is an interrelated set of measures to establish, ensure and maintain the necessary level of labor productivity, due to the use of professional skills of personnel, carried out through systematic control and targeted impact on the conditions and factors affecting productivity and product quality. In other words, it is a purposeful process of influencing the level of business reputation of personnel, carried out during the creation and use of products (services), in order to establish, ensure, and maintain the necessary level of productivity and the use of professional qualities of personnel.

The competitiveness of any product is determined by the totality of only those of its properties that are of interest to the buyer and provide the satisfaction of this need. Other parameters that go beyond the specified limits should not be taken into account in the evaluation.

For future owners, investors, creditors, and partners of an economic entity, the business reputation of its personnel is of undoubted interest.

It is clear that depending on its level, certain management decisions can be formed. In addition, the level of business reputation of the staff can be a primary factor in determining the sales price of the company.

It follows that the business reputation of the staff is the difference between the actual and standard level of labor productivity in a similar market sector.

As a result, the business reputation of the staff is positive, negative and zero.

Positive business reputation of the staff–increased activity to the actual net revenue compared to the net revenue that was performed within the production plan and which was not affected by the performance of the staff who completed the production plan below the norm, due to a lower level of application of professional skills or other factors.

Negative business reputation of personnel –a decrease in activity to actual net revenue compared to net revenue that was performed within the production plan and was not affected by the performance of personnel who completed the production plan above the norm, due to more intensive and effective use of professional skills or other factors.

Zero employee goodwilloccurs when the actual net revenue is equal to the net revenue that is performed within the production plan, or when the positive employee goodwill is equal to the negative employee goodwill.

To solve the problem of assessing the business reputation of the staff and to refute the regulatory guidance «the composition of intangible assets does not include the intellectual and business qualities of the organization’s personnel, their qualifications, and ability to work, since they are inseparable from their carriers and cannot be used without them» below is the author’s methodology for evaluating the performance of industrial and production personnel (standard-production methodology).

Comprehensive methodology for evaluating the result of industrial and production personnel (standard-production methodology)1

The developed comprehensive methodology for evaluating the resulting of industrial and production personnel (standard-production methodology) contributes to the formation of accounting and information support for the analysis of the activities of both structural divisions, centers of responsibility, business segments, and commercial organizations as a whole [55Filatov EA. Methodology for forming information about costs and expenses. Izvestiya IGEA. Irkutsk: BSUEL Publishing House. 2007; 1(51):16-19.-77Filatov EA. Methodology of forming the value of the business reputation of human capital in order to assess the capitalization of companies. European Social Science Journal. Moscow: Publishing House of the International Research Institute. 2011; 7:447-453.].

According to the author, the assessment of the effectiveness of the (industrial and production personnel) IPP is a mutually linked set of measures to establish, ensure, and maintain the necessary level of labor productivity, due to the use of professional skills of personnel, carried out through systematic control and targeted impact on the conditions and factors affecting the productivity and quality of products.

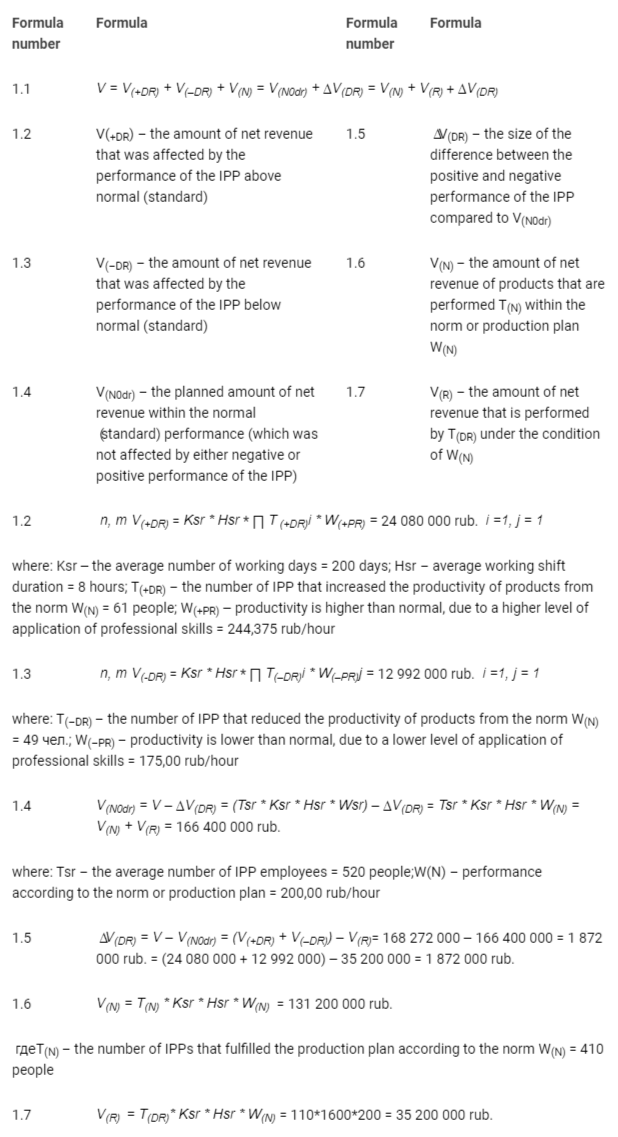

The initial formula for the formation of the author’s methodology (the methodology for the formation of the evaluation of the resulting IPP – standard-production).

V = Tsr * Ksr * Hsr * Wsr (1)

The formulas that reveal the essence of the standard production method are presented in Table 1.

Table 1: Formulas that reveal the essence of the standard-production methodology.

Based on the identified impact of productivity other than the planned IPP on net revenue (Table 2), the aggregate coefficient of the impact of productivity other than the planned (standard) on net revenue is derived.

Table 2: Calculation of net revenue.

KDRV = (∆V(DR) / V)*100 % (2)

where: KDRV– the cumulative effect of non-normalized productivity on net revenue, %.

The total coefficient of the influence of non-normalized productivity on net revenue can in turn be decomposed into the coefficients of the influence of positive and negative productivity on net revenue (formulas 3, 4).

К(+DR) – excess productivity impact factor on net revenue, %

К(–DR) – performance impact factor below production plan on net revenue, %

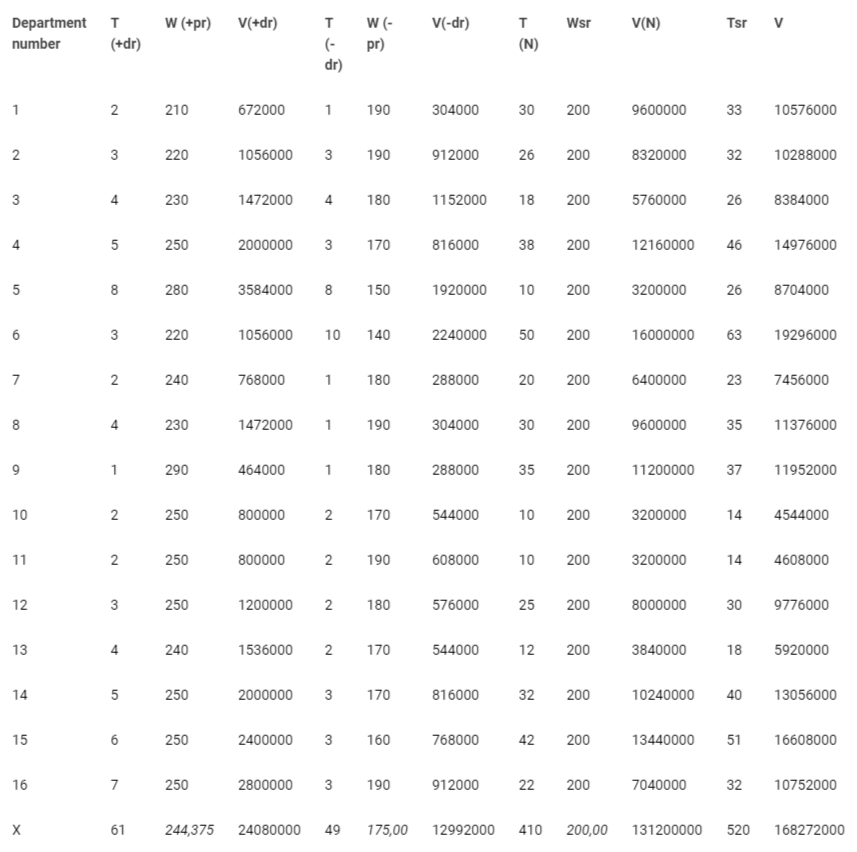

The approbation of the methodology of forming the business reputation of the staff is presented in Tables 3-8 to reflect the excess of the positive business reputation of the staff over the negative one.

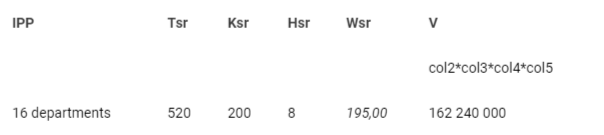

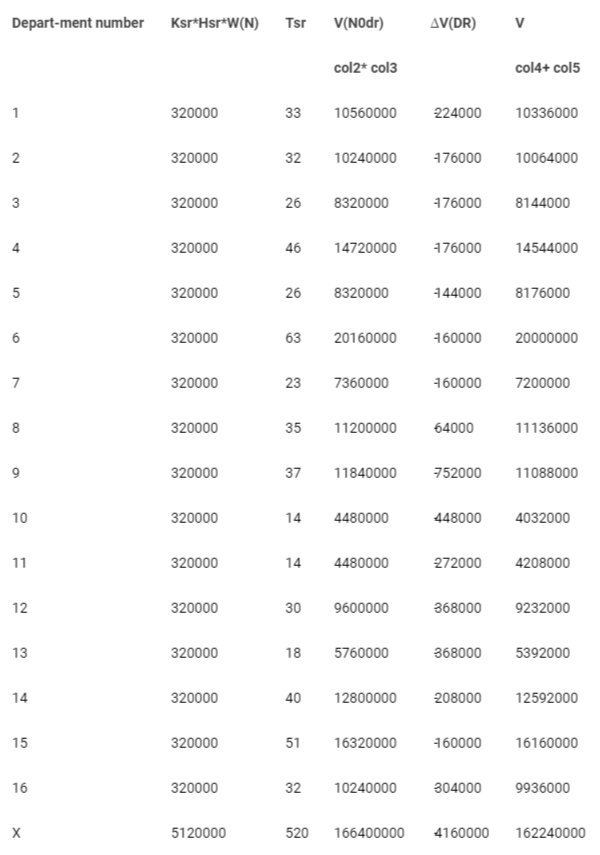

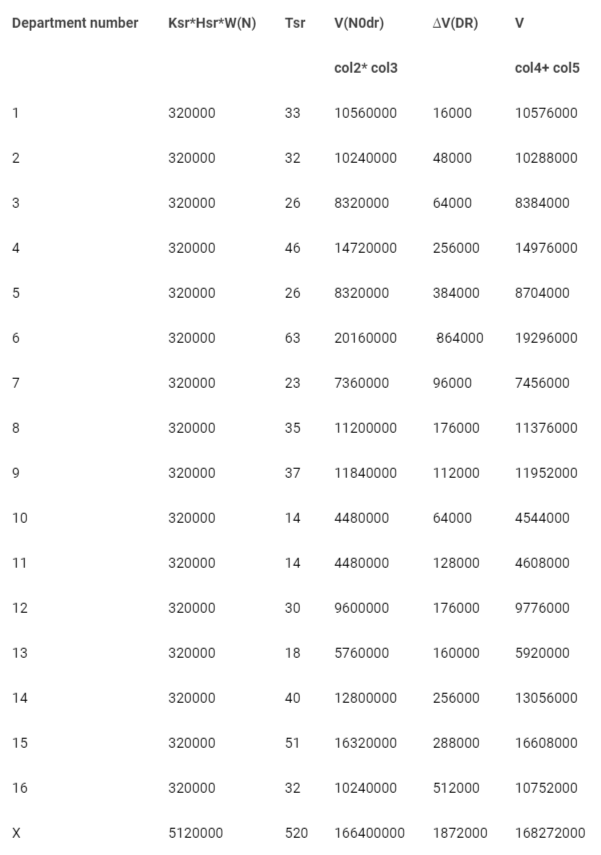

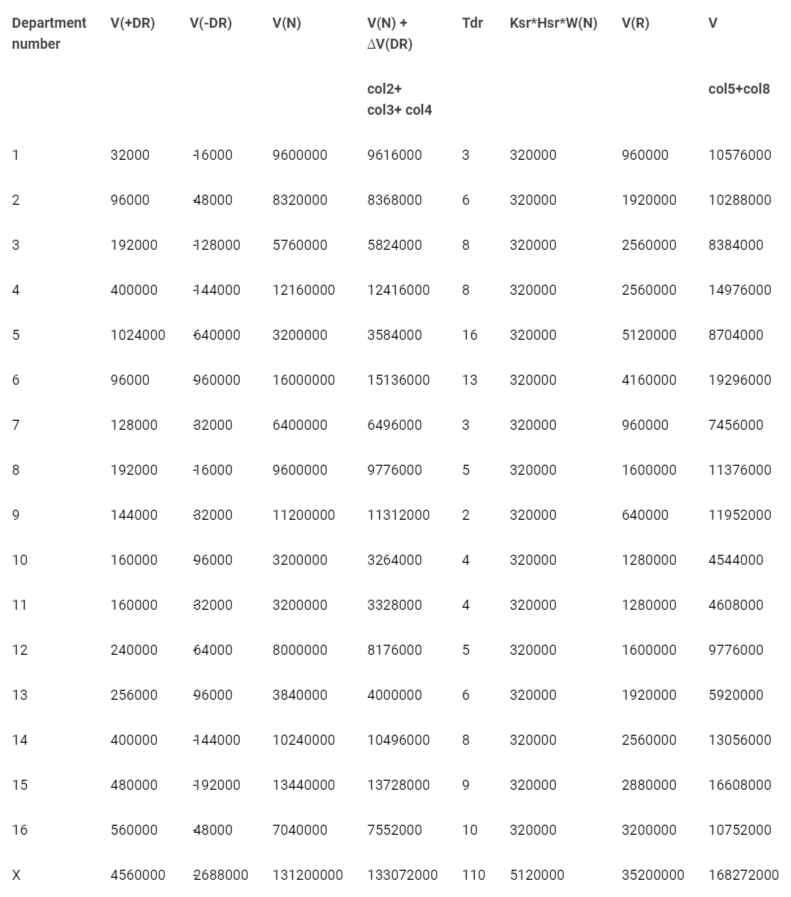

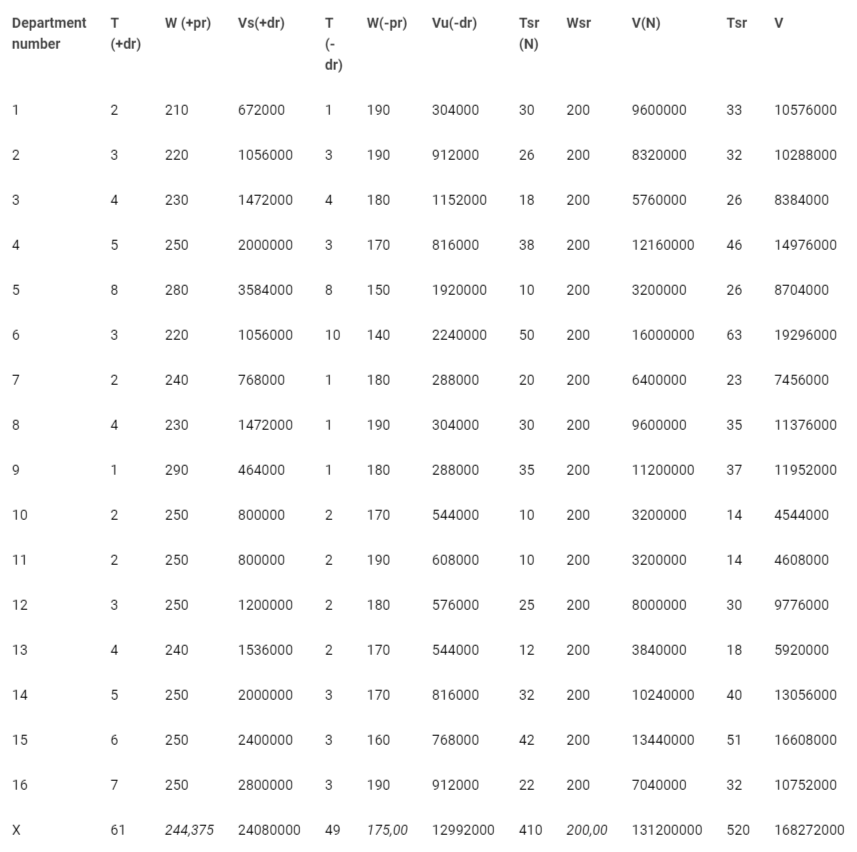

Table 3: Initial data for the formation of the methodology.

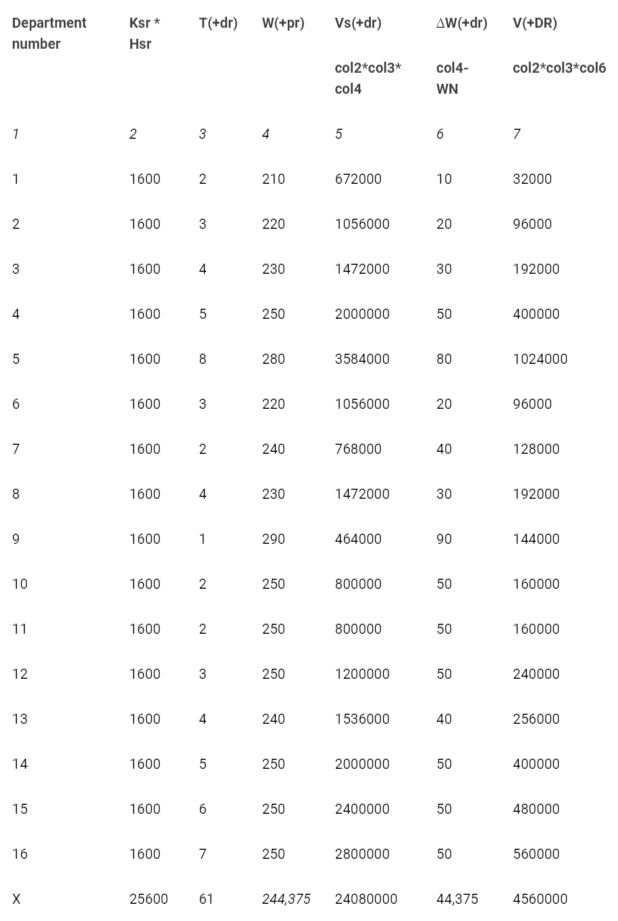

Table 4: Calculation of the amount of net revenue affected by the positive business reputation of the IPP.

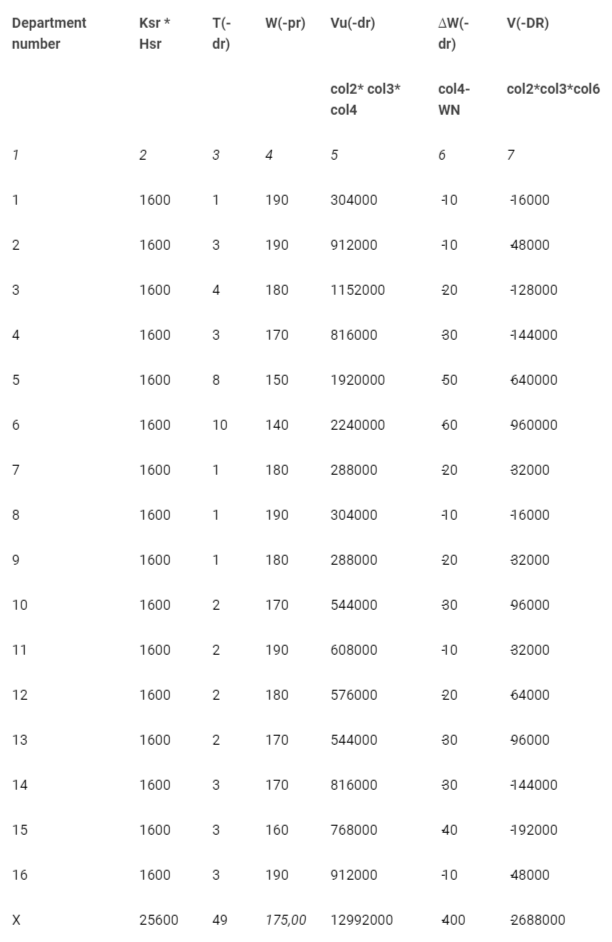

Able 5: Calculation of the amount of net revenue affected by the negative business reputation of the IPP.

Table 6: Calculation of the amount of net revenue that was not affected by the business reputation of the IPP.

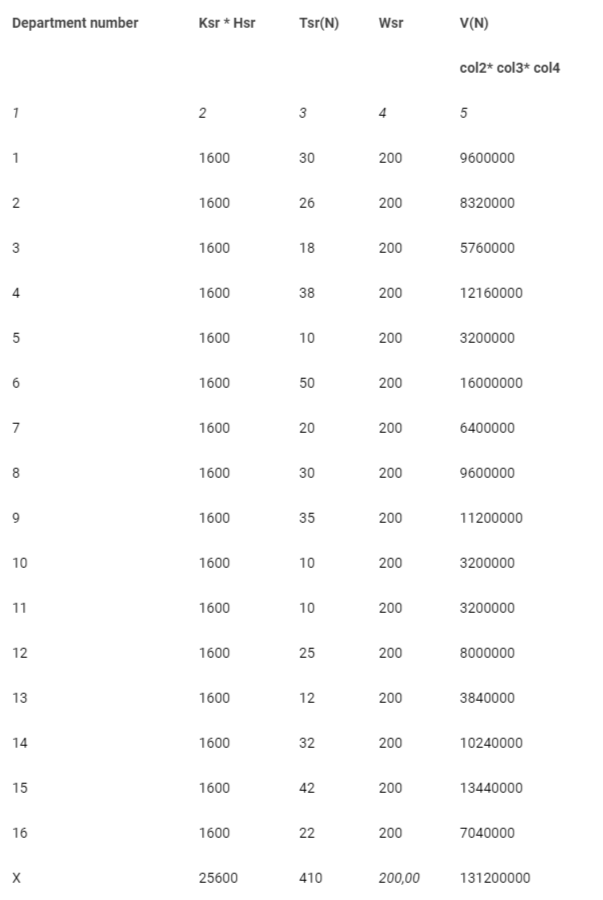

Table 7: Calculation of the amount of net revenue affected by the business reputation of the IPP.

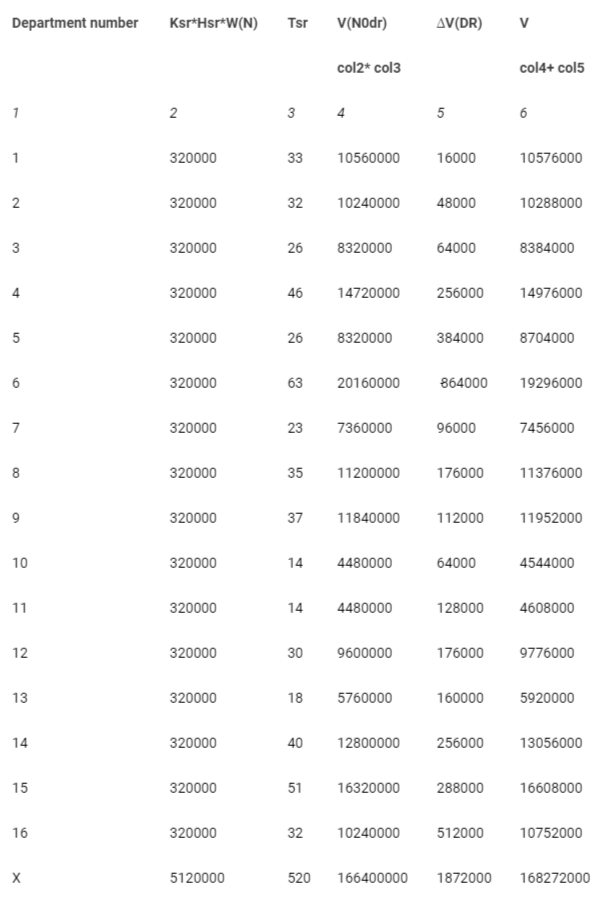

Table 8: Calculation of the amount of net revenue affected by the business reputation of the IPP.

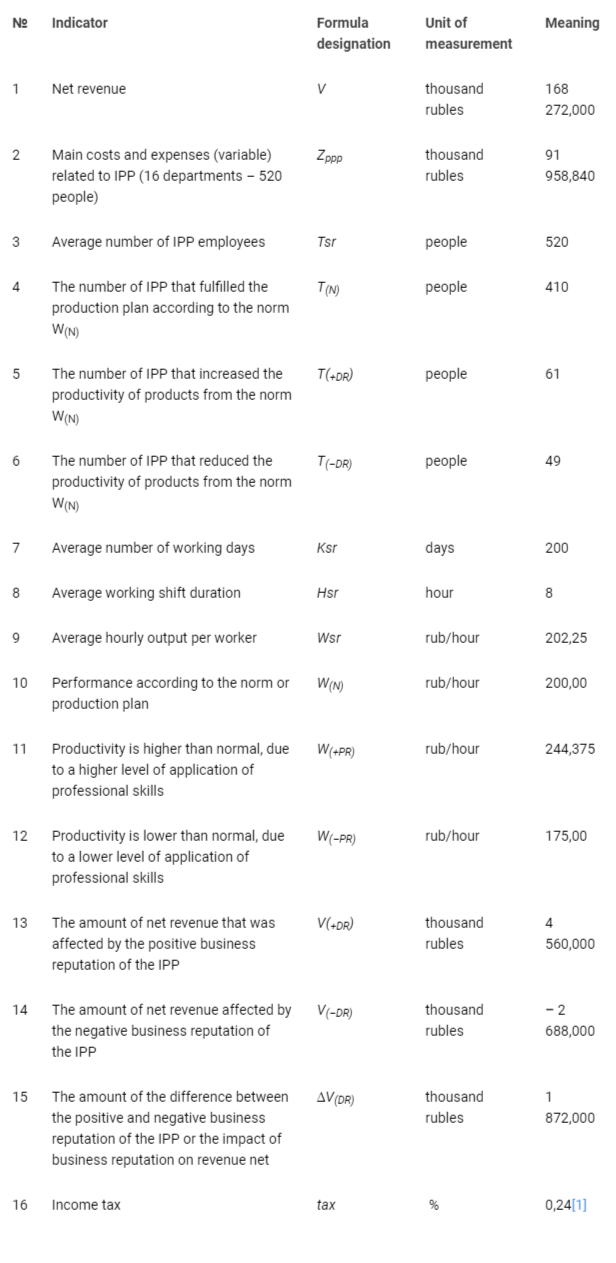

Final indicators based on the approbation of the presented methodology according to Example No. 1:

V = 168 272 000 rub.;

V(+DR) = 4 560 000 rub.;

V(–DR) = – 2 688 000 rub.;

∆V(DR) = 1 872 000 rub.;

KDRV = + 1,11 %;

К(+DR) = + 2,71 %;

К(–DR) = – 1,60 %,

by:

T(N) = 410 people; W(N) = 200,00 rub/hour;

T(+DR) = 61 people; W(+PR)= 244,375 rub/hour;

T(–DR) = 49 people; W(–PR) = 175,00 rub/hour;

Tsr = 520 people.

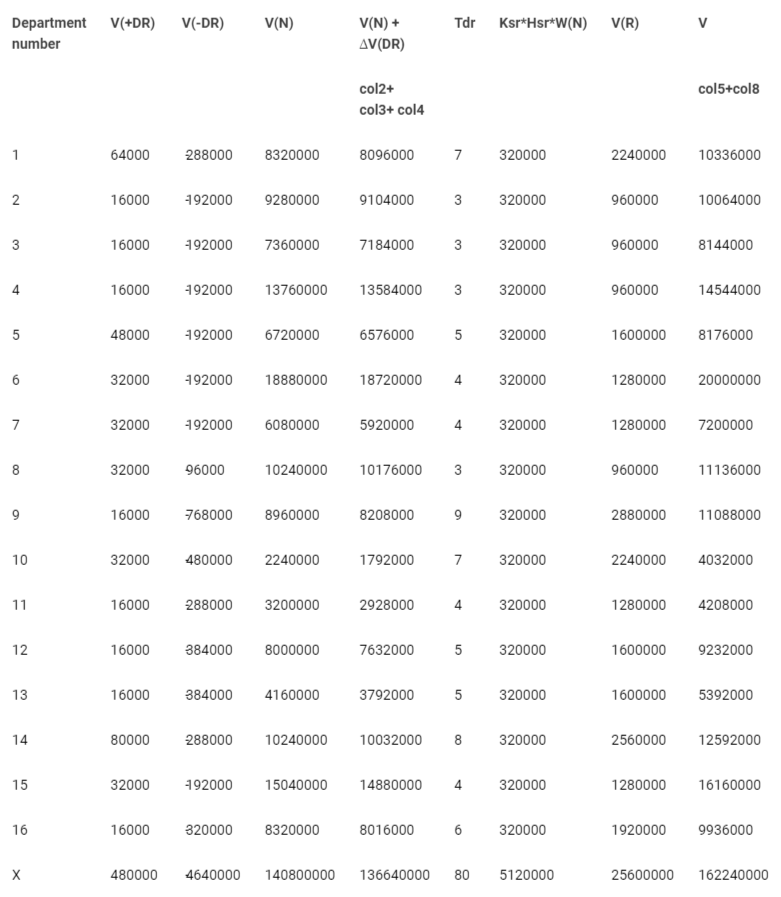

The approbation of the presented methodology of forming the business reputation of the staff is presented to reflect the excess of the negative business reputation of the staff over the positive one is presented in Tables 9-14.

Table 9: Initial data for the formation of the methodology.

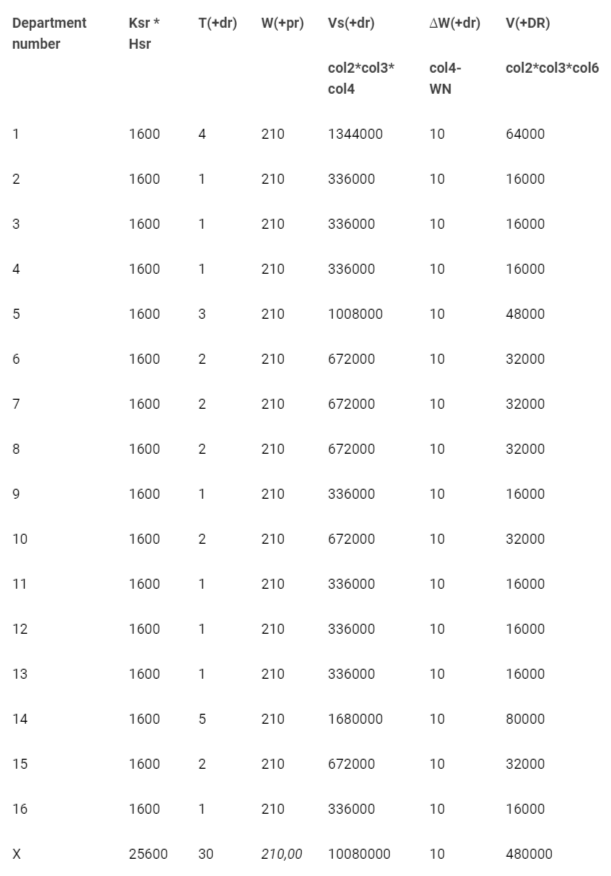

Table 10: Calculation of the amount of net revenue affected by the positive business reputation of the IPP.

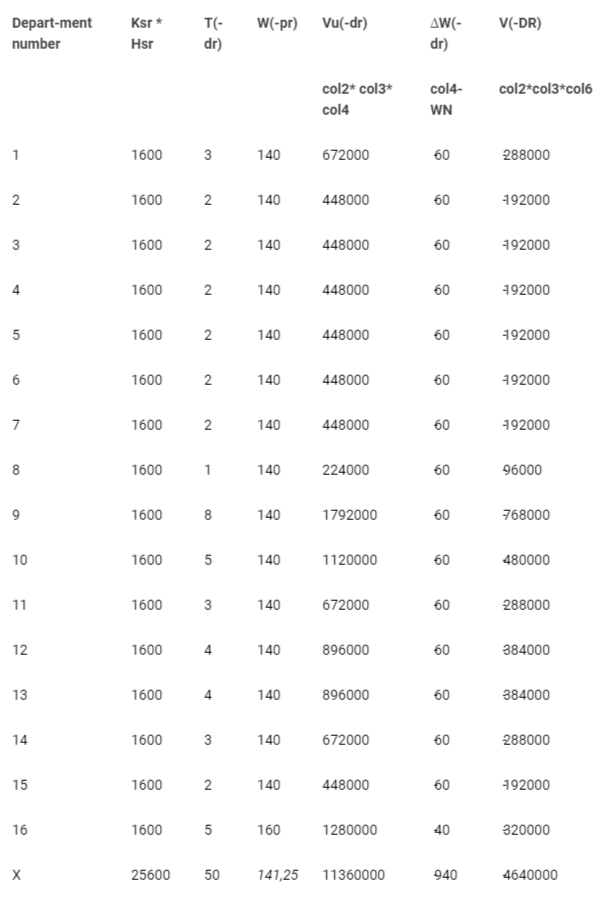

Table 11: Calculation of the amount of net revenue affected by the negative business reputation of the IPP.

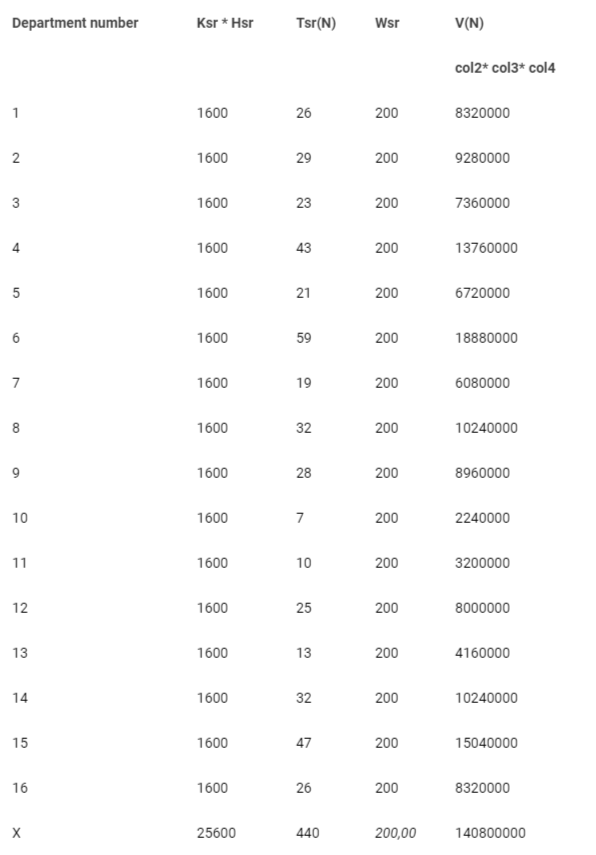

Table 12: Calculation of the amount of net revenue that was not affected by the business reputation of the IPP.

Table 13: Calculation of the amount of net revenue affected by the business reputation of the IPP.

Table 14: Calculation of the amount of net revenue affected by the business reputation of the IPP.

Final indicators based on the approbation of the presented methodology according to Example No. 2:

V = 162 240 000 rub.;

V(+DR) = 480 000 rub.;

V(–DR) = – 4 640 000 rub.;

∆V(DR) = – 4 160 000 rub.;

KDRV = – 2,56 %;

К(+DR) = + 0,30 %;

К(–DR) = – 2,86 %,

by:

T(N) = 440 people; W(N) = 200,00 rub/hour;

T(+DR) = 30 people; W(+PR)= 210,00 rub/hour;

T(–DR) = 50 people; W(–PR) = 175,00 rub/hour;

Tsr = 520 people.

It should be noted that the problem of managing the company’s value is put in the foreground before the management. In the perfectly competitive markets of the world, there is an increase in the capitalization of well-known companies. For future owners, investors, creditors, and partners of an economic entity, the assessment of the productivity of its personnel is of undoubted interest. It is clear that depending on its level, certain management decisions can be formed.

The proposed standard-production methodology, based on the cost-benefit ratio, is one of the ways to assess the effectiveness of management, regardless of the form of ownership and the organizational and legal form of the organization. The co-measurement of costs and all the diverse results of production and economic activity implies the need to measure in monetary form not only costs but also the results of this activity. Currently, there is a need to apply the proposed author’s assessment for such a level of management as an organization – the main subject of market relations. It is necessary to reorient the world theory and the accumulated practical experience in this area to solve new problems for making managerial decisions on this basis. Therefore, a better performance assessment is an effective tool for increasing the transparency and efficiency of the organization and its structural divisions.

Application of the variable cost allocation method in the standard-production methodology

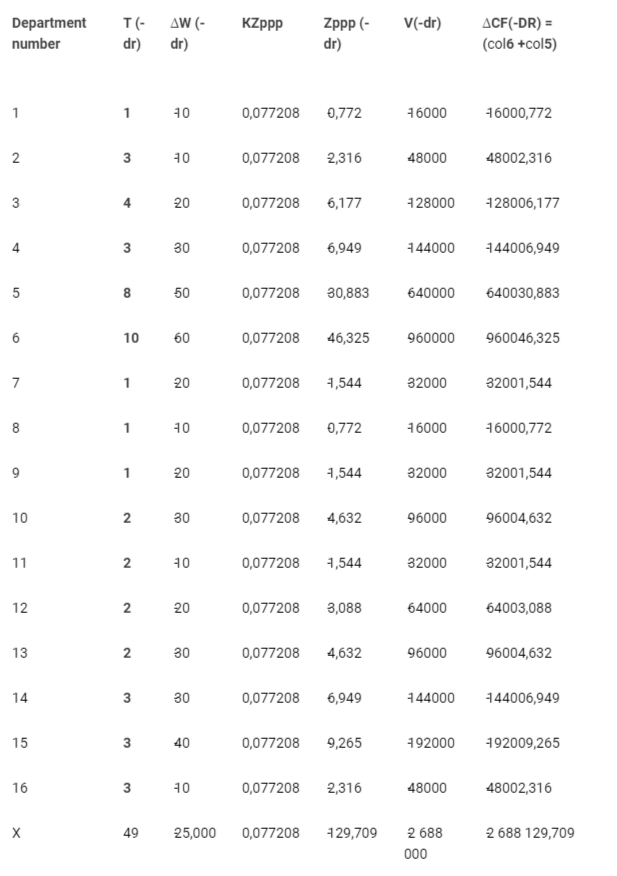

When determining the limits of the company’s growth, it is necessary to use the author’s methodology to determine the change in cash flow from current activities under the influence of the business reputation factor of the IPP (Table 15).

Table 15: Source data.

Testing of the determination of changes in cash flow from current activities under the influence of the business reputation factor of the IPP is presented in the formulas and Tables 16-20.

Table 16: Calculation of the amount of net revenue affected by the business reputation of the IPP.

Table 17: Calculation of the amount of net revenue affected by the business reputation of the IPP.

Table 18: Calculation of net revenue.

Table 19: Calculation of the amount of change in cash flow from current activities affected by the positive business reputation of the IPP.

Table 20: Calculation of the amount of change in cash flow from current activities affected by the negative business reputation of the IPP.

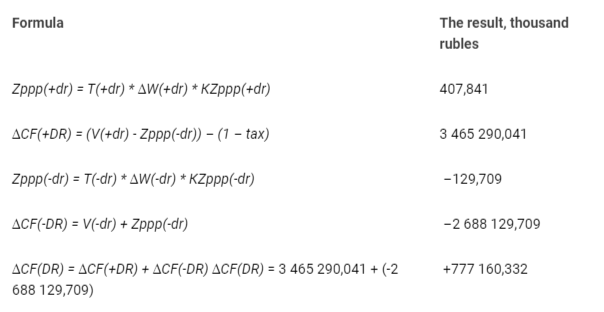

The calculation of the net revenue, which was affected by the positive business reputation of the IPP, is given in formula 5 (4 560 000 rub.).

V(+DR) = Ksr * Hsr * T(+dr) * ∆W(+dr) =

Ksr * Hsr * T(+dr) * (W(+pr) – W(N)) (5)

The calculation of the amount of net revenue affected by the negative business reputation of the IPP is given in formula 6 (–2 688 000 rub.).

V(–DR) = Ksr * Hsr * T(–dr) * ∆W(–dr) =

Ksr * Hsr * T(–dr) * (W(–pr) – W(N)) (6)

The calculation of the amount of net revenue, which was not affected by the business reputation of the IPP, is given in formula 7 (131 200 000 rub.).

V(N) = Ksr * Hsr * Tsr(N) * Wsr(7)

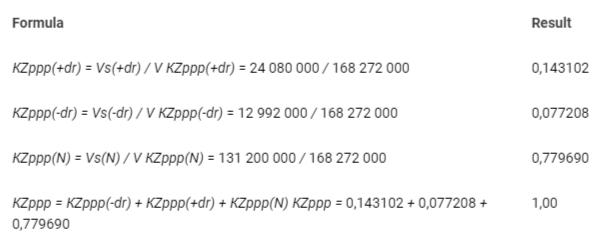

КZppp = Zppp / (Tsr* W(N)) (8)

Variable cost distribution coefficients (КZppp) are calculated as the ratio of the amount of revenue that was affected in a certain way by business reputation to the total amount of revenue (Tables 21, 22).

Table 21: Calculation of variable cost distribution coefficients.

Table 22: Calculation of variable costs associated with changes in cash flow from current activities under the influence of the business reputation factor IPP.

where:

∆CF(DR) – change in cash flow (the difference between the amounts of receipts and payments) from current activities under the influence of the business reputation factor IPP;

∆CF(+DR) – positive cash flow resulting from the application of a higher level of application of the professional skills of the IPP compared to the norm or production plan;

∆CF(-DR) – negative cash flow resulting from the application of a lower level of application of the professional skills of the IPP compared to the norm or production plan.

It should be noted that the problem of managing the company’s value is put in the foreground before the management. In the perfectly competitive markets of the world, there is an increase in the capitalization of well-known companies. As a result, it is possible to manage the process of forming a business reputation only after its specific measurement, since ignoring the value of the business reputation of the company’s human capital limits the objectivity of making decisions on investing in the company’s business. In addition, effective business reputation management is an effective tool for increasing the transparency and efficiency of the organization and its structural divisions. For the practical application of this author’s methodology, it is necessary to make appropriate changes to international financial reporting standards and recommend the use of this methodology to audit companies during the next audit [88Filatov EA. Application of the variable cost distribution method in the standard-production methodology. Izvestiya IGEA. Irkutsk: Publishing House of BSUEL. 2007; 6(56):37-41.].

At the same time, it should be noted that knowledge and information are very critical in terms of their application. It is well known that many firms have gaps between what they know and what they do. Therefore, when assessing the potential profitability of a company, it is necessary to take into account not only its capitalization, the dynamics of consumer requirements, and so on, but also, first of all, the business reputation of the company’s human capital.

As a result of the study, the following tasks were solved:

The author’s conceptual apparatus for assessing the business reputation of industrial and production personnel is presented, which allows to formulate the types of business reputation of industrial and production personnel.

A comprehensive methodology for evaluating the performance of industrial and production personnel (the standard-production methodology) is presented, which contributes to the formation of accounting and information support for the analysis of the activities of both structural divisions, responsibility centers, business segments, and commercial organizations as a whole. The author’s standard-production methodology makes it possible to assess the business reputation of industrial and production personnel.

The use of the author’s methodology is necessary for:

Owners of commercial organizations – to control the process of increasing the company’s value;

Managers of commercial organizations – in order to optimize management decision-making processes;

Employees of commercial organizations – when determining the coefficient of each employee’s personal contribution to the company’s growth;

Investors – in order to consider the development prospects of organizations when making decisions about the application of their investment flows;

To third-party organizations – when evaluating the reliability of potential partners.

The use of methodological aspects of the author’s methodology will improve both the effectiveness of the management system of commercial organizations and the effectiveness of their activities as a whole.

Business efficiency has always been the focus of attention of managers, economists and researchers. This is an actual problem, it is the basic subject of the study of economic science and practice.

The global financial and economic crisis of 2020, which the author previously wrote about [99Filatov EA. Some main milestones in the formation of the ideology of globalization: economic aspects. Innovations and investments. Moscow: Publishing house of LLC Journal of Innovations and Investments. 2014; 1: 85-92.-1212Filatov EA. The Plans of the Big four masters of money. Humanitarian, socio-economic and social Sciences. Krasnodar: Science and education. 2021; 1:158-164.], the bursting of the financial bubble in the stock markets, the bankruptcy of many companies have put the problem of evaluating the effectiveness of the company’s activities in the center of attention of the world community of economists once again.

Filatov EA. Management of the production cost of an industrial enterprise. Bulletin of IrSTU. Irkutsk: Publishing House of IrSTU. 2006; 2(26):2;35-36.

Filatov EA. The need to assess the main part of the business value. Izvestiya IGEA. Irkutsk: Publishing House of BSUEL. 2007;2(52):96-97.

Filatov EA. Methodology for the formation of business reputation of administrative, managerial and service personnel (standard management). Bulletin of IrSTU. Irkutsk: publishing house of Irkutsk state technical university. 2007; 1:2(29);110-114.

Shchadov MI, Filatov EA. The Relevance of the methodology for the assessment of business reputation of the human capital of the organization. Vestnik of the Irkutsk. Irkutsk: publishing house of Irkutsk state technical university. 2007; 1:1(29); 241-242.

Filatov EA. Methodology for forming information about costs and expenses. Izvestiya IGEA. Irkutsk: BSUEL Publishing House. 2007; 1(51):16-19.

Filatov EA. Methods of formation of business reputation of industrial personnel system (standard production). Bulletin of IrSTU. Irkutsk: Irkutsk: publishing house of Irkutsk state technical university. 2007; 4(32):192-200.

Filatov EA. Methodology of forming the value of the business reputation of human capital in order to assess the capitalization of companies. European Social Science Journal. Moscow: Publishing House of the International Research Institute. 2011; 7:447-453.

Filatov EA. Application of the variable cost distribution method in the standard-production methodology. Izvestiya IGEA. Irkutsk: Publishing House of BSUEL. 2007; 6(56):37-41.

Filatov EA. Some main milestones in the formation of the ideology of globalization: economic aspects. Innovations and investments. Moscow: Publishing house of LLC Journal of Innovations and Investments. 2014; 1: 85-92.

Filatov EA. Forecast of the beginning of the fundamental global financial and economic crisis of the third millennium. Management of economic systems: electronic scientific journal-Kislovodsk: Publishing House of LLC "D-Media". 2019; 10.

Filatov EA. the Analysis of international economic and financial crises. Management of economic systems: electronic scientific journal. Kislovodsk: Izd-vo OOO "E-Media". 2019; 11.

Filatov EA. The Plans of the Big four masters of money. Humanitarian, socio-economic and social Sciences. Krasnodar: Science and education. 2021; 1:158-164.

EA F. A Comprehensive Methodology for Assessing the Business Reputation of Industrial and Production Personnel. IgMin Res. Nov 22, 2023; 1(1): 081-093. IgMin ID: igmin120; DOI:10.61927/igmin120; Available at: www.igminresearch.com/articles/pdf/igmin120.pdf

Address Correspondence: Filatov EA, Candidate of Economic Sciences, Leading Researcher, Irkutsk Scientific Center of the Siberian Branch of the Russian Academy of Sciences, 664033, Irkutsk, Lermontov str., 134, Russia, Email: [email protected]

How to cite this article: EA F. A Comprehensive Methodology for Assessing the Business Reputation of Industrial and Production Personnel. IgMin Res. Nov 22, 2023; 1(1): 081-093. IgMin ID: igmin120; DOI:10.61927/igmin120; Available at: www.igminresearch.com/articles/pdf/igmin120.pdf

Table 3: Initial data for the formation of the methodology....

Table 4: Calculation of the amount of net revenue affected ...

able 5: Calculation of the amount of net revenue affected ...

Table 6: Calculation of the amount of net revenue that was ...

Table 7: Calculation of the amount of net revenue affected ...

Table 8: Calculation of the amount of net revenue affected ...

Table 9: Initial data for the formation of the methodology....

Table 10: Calculation of the amount of net revenue affected ...

Table 11: Calculation of the amount of net revenue affected ...

Table 12: Calculation of the amount of net revenue that was ...

Table 13: Calculation of the amount of net revenue affected ...

Table 14: Calculation of the amount of net revenue affected ...

Table 15: Source data....

Table 16: Calculation of the amount of net revenue affected ...

Table 17: Calculation of the amount of net revenue affected ...

Table 18: Calculation of net revenue....

Table 19: Calculation of the amount of change in cash flow f...

Table 20: Calculation of the amount of change in cash flow f...

Table 21: Calculation of variable cost distribution coeffici...

Table 22: Calculation of variable costs associated with chan...

Table 1: Formulas that reveal the essence of the standard-p...

Filatov EA. Management of the production cost of an industrial enterprise. Bulletin of IrSTU. Irkutsk: Publishing House of IrSTU. 2006; 2(26):2;35-36.

Filatov EA. The need to assess the main part of the business value. Izvestiya IGEA. Irkutsk: Publishing House of BSUEL. 2007;2(52):96-97.

Filatov EA. Methodology for the formation of business reputation of administrative, managerial and service personnel (standard management). Bulletin of IrSTU. Irkutsk: publishing house of Irkutsk state technical university. 2007; 1:2(29);110-114.

Shchadov MI, Filatov EA. The Relevance of the methodology for the assessment of business reputation of the human capital of the organization. Vestnik of the Irkutsk. Irkutsk: publishing house of Irkutsk state technical university. 2007; 1:1(29); 241-242.

Filatov EA. Methodology for forming information about costs and expenses. Izvestiya IGEA. Irkutsk: BSUEL Publishing House. 2007; 1(51):16-19.

Filatov EA. Methods of formation of business reputation of industrial personnel system (standard production). Bulletin of IrSTU. Irkutsk: Irkutsk: publishing house of Irkutsk state technical university. 2007; 4(32):192-200.

Filatov EA. Methodology of forming the value of the business reputation of human capital in order to assess the capitalization of companies. European Social Science Journal. Moscow: Publishing House of the International Research Institute. 2011; 7:447-453.

Filatov EA. Application of the variable cost distribution method in the standard-production methodology. Izvestiya IGEA. Irkutsk: Publishing House of BSUEL. 2007; 6(56):37-41.

Filatov EA. Some main milestones in the formation of the ideology of globalization: economic aspects. Innovations and investments. Moscow: Publishing house of LLC Journal of Innovations and Investments. 2014; 1: 85-92.

Filatov EA. Forecast of the beginning of the fundamental global financial and economic crisis of the third millennium. Management of economic systems: electronic scientific journal-Kislovodsk: Publishing House of LLC "D-Media". 2019; 10.

Filatov EA. the Analysis of international economic and financial crises. Management of economic systems: electronic scientific journal. Kislovodsk: Izd-vo OOO "E-Media". 2019; 11.

Filatov EA. The Plans of the Big four masters of money. Humanitarian, socio-economic and social Sciences. Krasnodar: Science and education. 2021; 1:158-164.

Scan and get link

Scan and get link